The Fiscal Frontline: Can Europe Afford to Rearm While Cutting Debt?

The Unavoidable Collision

It is early 2026, and the European Union stands at a defining economic crossroads. On one side, the geopolitical threat level remains critical, forcing member states to accelerate military modernization and ammunition production. On the other, the reinstated Stability and Growth Pact (SGP) has snapped back into force, placing countries like France, Italy, and Belgium in a fiscal straitjacket just as defense bills come due.

The era of suspended fiscal rules, a legacy of the pandemic and energy crisis, is over. Brussels is once again enforcing the Maastricht criteria—capping deficits at 3% and debt at 60% of GDP—creating a direct conflict with NATO's rising floor for defense spending, which many experts argue must now move well beyond the 2% target.

Key Data: The Scale of the Gap

The numbers paint a stark picture of the challenge facing Finance Ministers across the continent:

- The Investment Gap: Defense analysts estimate the EU faces a shortfall of approximately €75–€100 billion annually to meet current strategic autonomy goals and replenish depleted stockpiles.

- Debt Loads: Public debt remains stubbornly high in key economies. France faces a debt-to-GDP ratio estimated at 114%, while Italy remains critical above 135%. Belgium continues to grapple with a ratio around 103%.

- The Deficit Hurdle: Under the Excessive Deficit Procedure (EDP), member states with deficits above 3% face mandated structural adjustments of 0.5% of GDP per year—money that cannot easily be diverted to defense without severe cuts to welfare or infrastructure.

The Debate: Financial Engineering for Security

With national budgets stretched to breaking point, the debate has shifted from "should we spend?" to "how do we account for it?". Three primary mechanisms are currently dominating closed-door meetings in Brussels and Frankfurt:

1. The "Defense Bond" Proposal

Led by France and supported by Baltic states, there is a renewed push for joint EU borrowing specifically for defense—effectively "Eurobonds" for security. Proponents argue this would shield national credit ratings and lower borrowing costs. However, resistance from fiscal hawks in Germany and The Netherlands remains fierce, fearing it establishes a permanent transfer union by the back door.

2. Off-Balance-Sheet Vehicles

A more technical, yet likely, solution involves Special Purpose Vehicles (SPVs). Similar to the pandemic-era SURE fund, these would allow defense spending to be categorized differently, potentially excluding specific military investments from the deficit calculations used for the Excessive Deficit Procedure. This "golden rule" for defense investment is gaining traction, even among fiscal conservatives who recognize the security existentialism.

3. EIB Mandate Expansion

Pressure is mounting on the European Investment Bank (EIB) to radically alter its lending criteria. Historically hesitant to fund defense (beyond dual-use technology), a 2026 mandate change could unlock billions in low-interest loans for the defense industry, bypassing direct sovereign debt issuance.

Outlook: A Compromise of Necessity

The status quo is untenable. For Europe to become a credible security actor without triggering a bond market crisis in Rome or Paris, a compromise is inevitable. We expect a modified interpretation of the fiscal rules to emerge by Q2 2026—one that does not give a blank check for spending, but acknowledges that security is a prerequisite for fiscal stability, not its enemy.

Europe cannot default on its defense, nor can it default on its debt. Track the real-time impact on our live EU Debt Clock.

Further Reading

Analysis and data you might have missed

Europe’s Debt Burden in 2026: Which EU Countries Are Under the Most Pressure?

Europe’s public debt is not spread evenly. This data-backed analysis explains why total debt and debt-to-GDP tell two different stories about fiscal pressure in the EU.

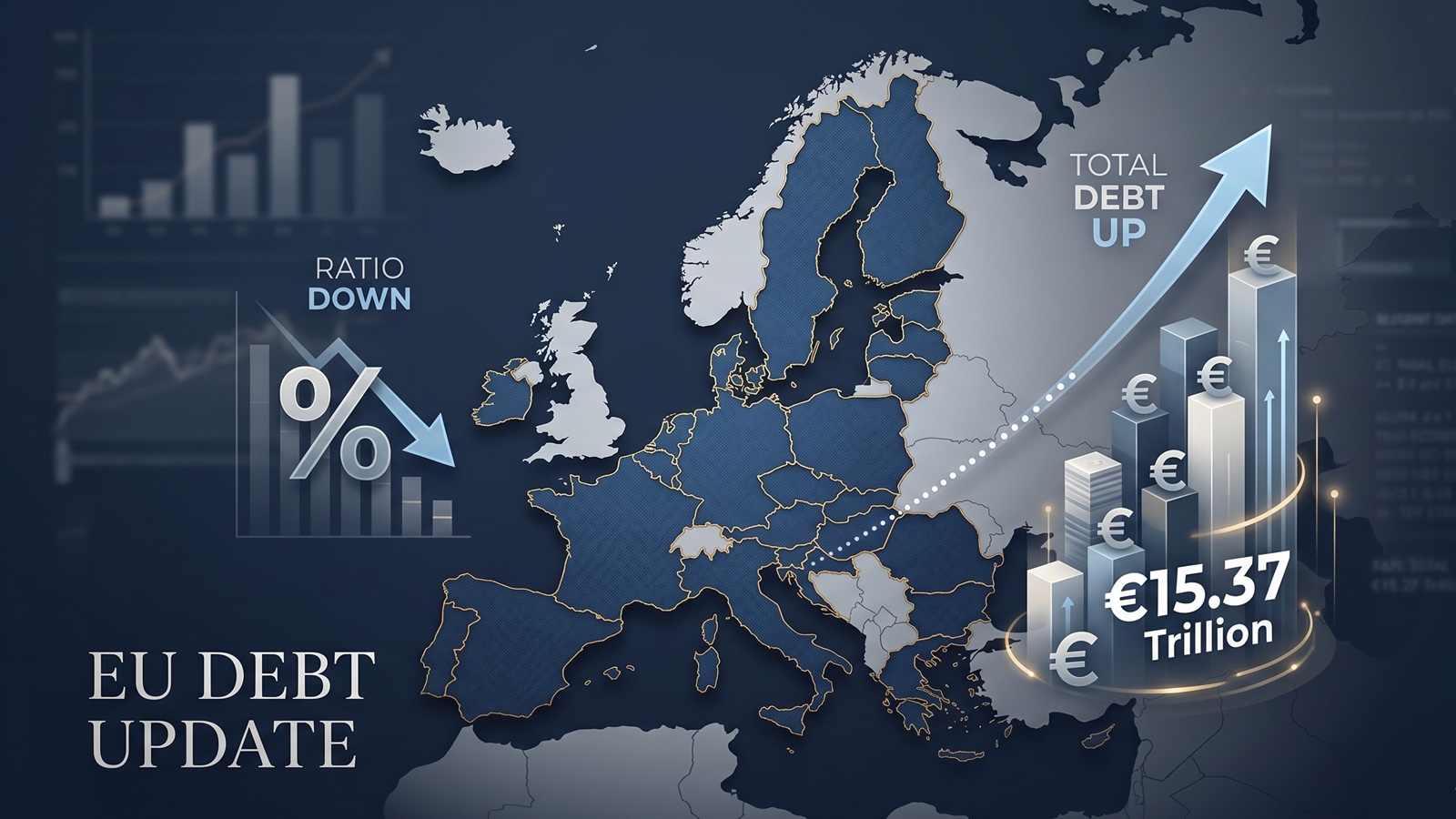

EU debt update: the ratio fell, but the pile still grew to €15.37tn

The latest Eurostat release offers a picture that looks calmer than it really is. The EU debt ratio edged down in late 2025, but the total stock of government debt still rose to more than €15.37tn.

EU Debt Explained: Why Adding It All Up Helps, and Misleads

Add together the public debt of all 27 EU countries and the total comes to more than €15 trillion. That number is useful, especially on a live map, but it can also mislead because Europe does not borrow like a single country.

Europe’s debt isn’t exploding — but something feels different in 2026

There’s no sudden debt crisis in Europe. But if you look closely, the direction is shifting. And that shift could matter more than the actual numbers.

The Dollar Dives, The Euro Thrives: A Silent Crisis for Europe's Debt Mountain?

As the Greenback stumbles, the Euro is gaining ground. While tourists cheer, Brussels holds its breath. We analyze how the shifting FX landscape threatens to rewrite the map of European sovereign debt.

Born with a €58,000 Mortgage? The 2026 Debt-per-Capita Map of Europe

New 2026 projections reveal a massive financial divide. While a Dutch citizen needs 9 months of work to pay off their share of the national debt, an Italian needs over 2 years.