The Digital Euro: Europe’s Leap Into the Future of Money

What is the digital euro?

The digital euro would be a central bank digital currency (CBDC) — euro money issued by the European Central Bank (ECB), but in digital form only. It would be as safe as cash because it is a direct claim on the central bank, not on a private bank.

You could keep it in a digital wallet (inside your banking app or a new ECB-backed app) and use it to pay in stores or online. The ECB says it should work online and offline, so small payments would still be possible if the internet is down.

Why does Europe want it?

- Monetary sovereignty: make sure euro payments stay under European control as crypto, stablecoins and Big Tech systems grow.

- Less dependence on non-EU networks: today, many cards and wallets run on non-European rails. A digital euro would be a European backbone.

- Future-proof money: other big economies are testing CBDCs; the EU doesn’t want to fall behind.

How might it work?

Design plans point to a two-tier model: the ECB issues digital euros; private banks and payment firms provide wallets and customer support. This way, the ECB does not replace banks.

Open questions the ECB and lawmakers still need to fix:

- Holding limits: to stop people moving too much money out of bank deposits during a crisis.

- Fees: will basic payments be free for users and shops?

- Privacy rules: how to stop crime while protecting normal users’ data.

Privacy and trust

Cash is private; digital payments leave a trail. The ECB says a digital euro will offer strong privacy, especially for small offline payments. Civil-rights groups worry about surveillance. Too little privacy reduces trust; too much privacy could make it hard to fight fraud and money laundering. Finding the right balance is key.

What could it mean for citizens?

- Universal acceptance: like cash, usable across the euro area.

- Financial inclusion: a simple wallet could help people without a bank account join digital payments.

- Resilience: if a private network fails, a state-backed option keeps payments running.

Trade-off: if it is too attractive to hold digital euros, banks could lose deposits, which might raise loan costs. That is why holding limits and design choices matter.

The global race

Over 100 countries are exploring CBDCs. China’s digital yuan is far along. The Bahamas, Nigeria and Jamaica have already launched. Europe’s project is slower and careful, but it would be one of the largest CBDC pilots in the world.

Big open questions

- Will it replace cash or only complement it? (Officials say cash will stay.)

- Will people trust a central-bank wallet as much as their bank’s app?

- Could governments set temporary limits in a crisis (for example, on very large transfers)?

- Could a successful digital euro boost the euro’s global role in trade and finance?

Bottom line

The digital euro could make payments faster, safer and more inclusive, and strengthen Europe’s independence. But it also raises hard questions about privacy and the role of banks. The choices Europe makes now will decide whether the digital euro becomes a trusted everyday tool or a controversial experiment.

Note: This explainer summarizes the public discussion around the ECB’s digital euro project as of 2025. It is educational content, not legal or financial advice.

Further Reading

Analysis and data you might have missed

Europe’s Debt Burden in 2026: Which EU Countries Are Under the Most Pressure?

Europe’s public debt is not spread evenly. This data-backed analysis explains why total debt and debt-to-GDP tell two different stories about fiscal pressure in the EU.

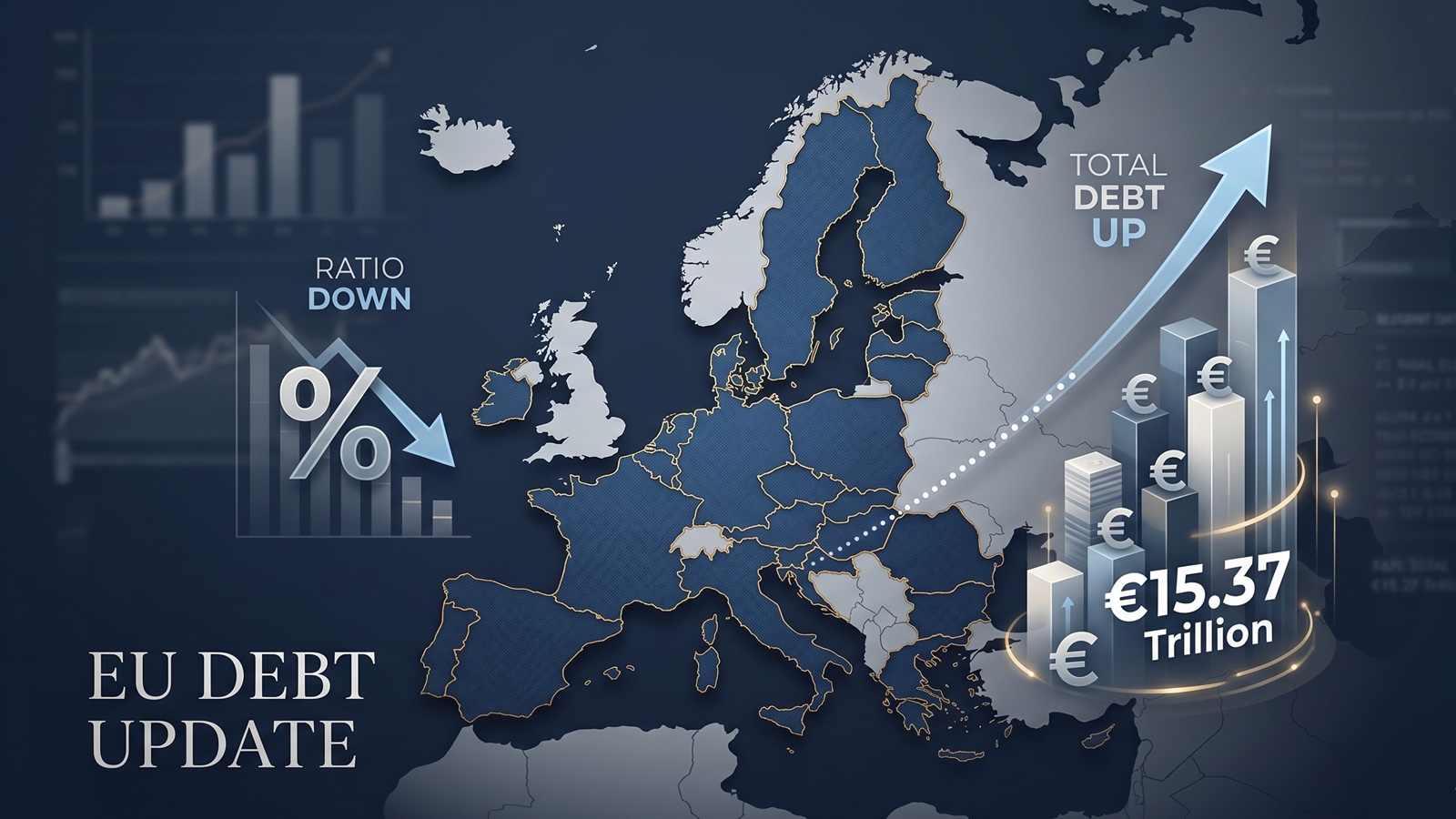

EU debt update: the ratio fell, but the pile still grew to €15.37tn

The latest Eurostat release offers a picture that looks calmer than it really is. The EU debt ratio edged down in late 2025, but the total stock of government debt still rose to more than €15.37tn.

EU Debt Explained: Why Adding It All Up Helps, and Misleads

Add together the public debt of all 27 EU countries and the total comes to more than €15 trillion. That number is useful, especially on a live map, but it can also mislead because Europe does not borrow like a single country.

Europe’s debt isn’t exploding — but something feels different in 2026

There’s no sudden debt crisis in Europe. But if you look closely, the direction is shifting. And that shift could matter more than the actual numbers.

The Dollar Dives, The Euro Thrives: A Silent Crisis for Europe's Debt Mountain?

As the Greenback stumbles, the Euro is gaining ground. While tourists cheer, Brussels holds its breath. We analyze how the shifting FX landscape threatens to rewrite the map of European sovereign debt.

Born with a €58,000 Mortgage? The 2026 Debt-per-Capita Map of Europe

New 2026 projections reveal a massive financial divide. While a Dutch citizen needs 9 months of work to pay off their share of the national debt, an Italian needs over 2 years.