Europe's Trillion-Euro Question: When Is National Debt an Investment?

The New Rules of Debt

In the quiet halls of Brussels and Berlin, a deeply ingrained economic dogma is dissolving. For decades, particularly within the eurozone, high national debt was seen as a moral failure, a sign of profligacy to be punished with austerity. The Maastricht Treaty's rigid 60% debt-to-GDP ratio was less a guideline than a gospel.

Then came the deluge: the 2008 financial crisis, a once-in-a-century pandemic, and a land war on the continent's eastern flank. Suddenly, the taps opened, and the debt-to-GDP ratios, meticulously tracked on sites like the EU Debt Map, exploded. Greece, already high, soared past 178%; Italy to 140%; France and Spain breached the 100% mark. Even frugal Germany saw its ratio jump.

This surge in borrowing has forced a continent to confront a question it has long avoided: Is all debt created equal? The emerging consensus is a resounding no.

There is a profound difference between borrowing to fund pension payments or current public salaries—consumption, in economic terms—and borrowing to build a productive asset. It is the difference, economists argue, between a credit card binge and a mortgage.

“The fundamental limit to public debt is not a magic number, but inflation,” said a senior economist at a major European think tank. “If you borrow money and use it to hire workers and buy materials that are already scarce, you just drive up prices. But if you borrow to invest in something that increases your future productive capacity, the debt can, in effect, pay for itself.”

This is the ‘Golden Rule’ of public finance: borrowing is justified if the return on the investment (i.e., future economic growth) is higher than the interest paid on the loan. As Europe stands at the precipice of its two greatest challenges since post-war reconstruction, this theory is being put to the test.

The 7 Trillion Challenge: Europe's 'Twin Transitions'

Europe's future competitiveness, its strategic autonomy, and its climate commitments rest on two colossal pillars: the Green Transition and the Digital Transition.

The investment required is staggering. The European Commission estimates that the Green Deal alone—the plan to make the EU climate-neutral by 2050—will require hundreds of billions in additional investment every year. This is not just about building solar panels and wind turbines; it's about retrofitting millions of buildings, redesigning the entire energy grid, and creating new supply chains for materials like green hydrogen and sustainable batteries.

Simultaneously, the digital transition demands massive capital. The pandemic and geopolitical tensions exposed Europe's dangerous reliance on other powers for critical technologies, from Taiwanese semiconductors to American cloud computing.

“We have a choice,” a high-level EU official noted, speaking on condition of anonymity. “We can either borrow to secure our own semiconductor supply, our 5G infrastructure, and our AI capabilities, or we can become a digital colony. The first option creates value. The second makes us a permanent vassal.”

These are not simple expenditures; they are foundational investments. A modern digital infrastructure 'crowds in' private investment. Companies are more likely to build a high-tech factory in a region with guaranteed gigabit fiber and a stable green energy grid. This synergy, proponents argue, creates a virtuous cycle of growth that raises GDP, thereby shrinking the relative size of the very debt that funded it.

Navigating the Debt Map

This new logic creates a complex landscape. A quick glance at the EU Debt Map reveals the disparities. On one end, you have countries like Estonia (19.6%) and Bulgaria (21.3%) with negligible debt. On the other, you have Greece (178.1%), Italy (140.6%), and France (110.6%).

The old logic would demand that Italy and Greece cease all borrowing and enter a period of painful austerity. The new logic asks a different question: What is the risk of not investing?

Take Italy. Its high debt is a serious vulnerability. But it also has an aging industrial base and is highly exposed to climate change and energy shocks. If Italy fails to borrow for green energy and digital modernization, its economy will stagnate. That stagnation will make its 140% debt burden truly unsustainable. In this scenario, not investing is the riskier path.

This is where the debate now lies. The question is not “How high is the debt?” but “What is the debt for?”

Germany, long the bastion of fiscal prudence (63.7%), is itself grappling with this. Its 'debt brake' (Schuldenbremse) written into its constitution, has been criticized for starving the country of public investment, leading to crumbling bridges and slow digital rollout. Even in Berlin, the conversation is shifting from if to how to fund the necessary green and digital upgrades without technically breaking the rules.

The Ghost in the Machine: Inflation

This new era of investment-led debt is not without its perils. The primary risk, which came roaring back in 2022, is inflation.

When governments inject billions into the economy, whether for consumption (like pandemic support checks) or investment (like building a battery factory), it increases demand. If that demand outstrips the economy’s ability to supply goods and services—if there aren't enough engineers, raw materials, or microchips—prices simply rise.

This is the real constraint. A country cannot simply print money to build its way to prosperity. The investment must be targeted, productive, and, crucially, timed to match the economy's capacity.

The other risk is the return of high interest rates. The 'Golden Rule' works beautifully when interest rates are near zero, as they were for most of the last decade. But as central banks raise rates to fight inflation, the cost of servicing that debt rises. A loan for a 30-year infrastructure project that seemed cheap at 0.5% interest becomes a heavy burden at 4%.

This is the tightrope Europe must walk. It must invest heavily to secure its future, but it must do so smartly, focusing on projects that deliver tangible, long-term productive growth, without overheating the economy in the present.

The old rules are gone. The new rules are still being written, not in treaties, but in the real-world laboratories of energy grids, data centers, and the unforgiving bond markets.

Further Reading

Analysis and data you might have missed

Europe’s Debt Burden in 2026: Which EU Countries Are Under the Most Pressure?

Europe’s public debt is not spread evenly. This data-backed analysis explains why total debt and debt-to-GDP tell two different stories about fiscal pressure in the EU.

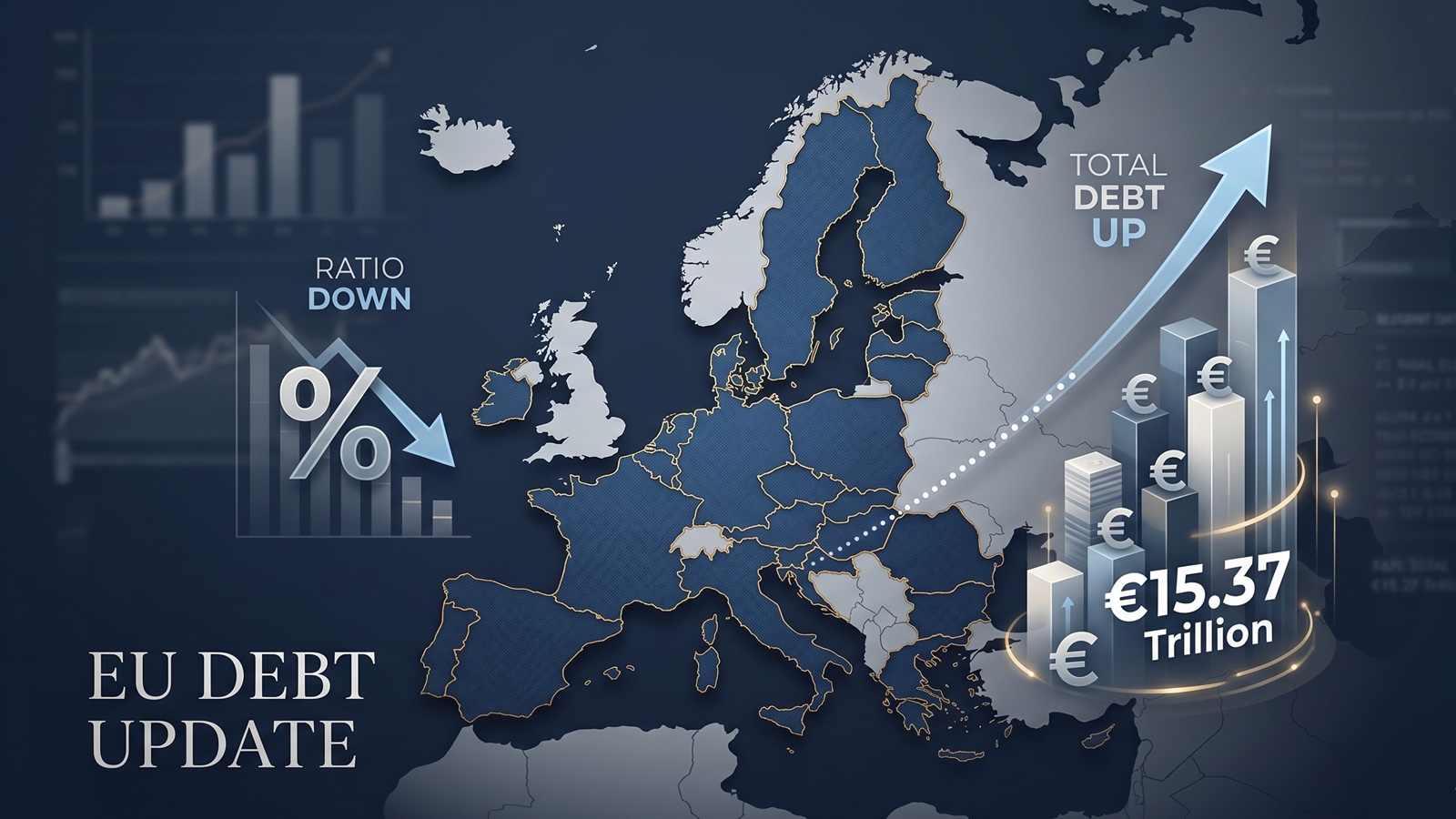

EU debt update: the ratio fell, but the pile still grew to €15.37tn

The latest Eurostat release offers a picture that looks calmer than it really is. The EU debt ratio edged down in late 2025, but the total stock of government debt still rose to more than €15.37tn.

EU Debt Explained: Why Adding It All Up Helps, and Misleads

Add together the public debt of all 27 EU countries and the total comes to more than €15 trillion. That number is useful, especially on a live map, but it can also mislead because Europe does not borrow like a single country.

Europe’s debt isn’t exploding — but something feels different in 2026

There’s no sudden debt crisis in Europe. But if you look closely, the direction is shifting. And that shift could matter more than the actual numbers.

The Dollar Dives, The Euro Thrives: A Silent Crisis for Europe's Debt Mountain?

As the Greenback stumbles, the Euro is gaining ground. While tourists cheer, Brussels holds its breath. We analyze how the shifting FX landscape threatens to rewrite the map of European sovereign debt.

Born with a €58,000 Mortgage? The 2026 Debt-per-Capita Map of Europe

New 2026 projections reveal a massive financial divide. While a Dutch citizen needs 9 months of work to pay off their share of the national debt, an Italian needs over 2 years.